Rabi 2026 has been a story of surplus production and commodity price fluctuations due to the looming geo-political scenario and natural calamity potentially impacting agri-inputs and crop production for the next season.

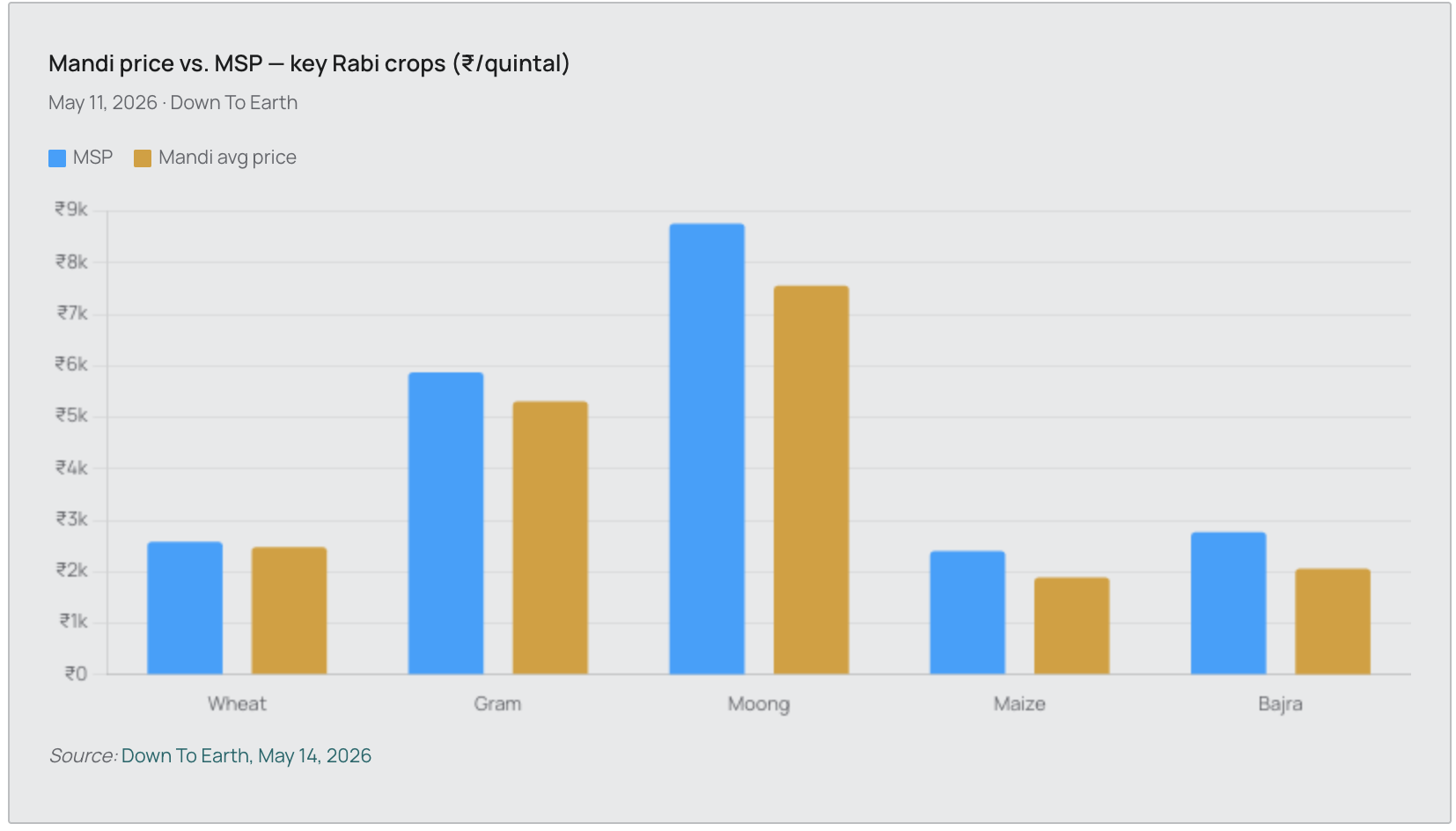

India’s Rabi 2025-26 season has produced a harvest 3.2% higher than last year (1,745.13 LMT, increase of 53 LMT, per the Ministry of Agriculture’s Second Advance Estimates). Across crops, wholesale mandi prices are trading significantly below their Minimum Support Prices (MSPs), impacting the procurement and loss of selling opportunity of the farmers.

Our analysis of MODIS data shows the positive deviation against the 5 year NDVI trend across India.

Reporting by Down To Earth, citing the Crop Weather Watch Group (CWWG) weekly report dated May 11, 2026, found that market prices for paddy, wheat, maize, bajra, pulses, and oilseeds were all recorded below their respective MSPs. Bajra shows the starkest gap at 25.55% below MSP (mandi average ₹2,066 against MSP of ₹2,775 per quintal). Maize is 21.29% below MSP at ₹1,889 per quintal. Among pulses, moong trades at ₹7,556 against an MSP of ₹8,768 — a 13.82% shortfall.

The government has approved MSP support to strengthen farmer incomes. In Karnataka, over 9,000 metric tonnes of sunflower will be procured for the Rabi season, with an MSP value exceeding ₹69 crore. In Maharashtra, the gram procurement limit for Rabi 2025–26 has been raised to 8 lakh metric tonnes, with a total MSP value of over ₹4,800 crore. The procurement period has also been extended by 30 days until May 29 for gram. These measures aim to ensure fair prices, reduce market risks, and build stability and trust in the agricultural sector.

Strengthening Procurement for Wheat

The overall procurement turned YoY-positive for the first time on ~May 12, after trailing for 40 consecutive days since April 1. Haryana’s 1.5 mt surplus has offset Madhya Pradesh’s 0.7 mt shortfall. MP narrowed its deficit sharply from −59% (April 30) to −9% (May 12); purchases continue until June 30. Virtually all Punjab procurement was under relaxed quality specs (URS) due to lustre loss from unseasonal rains and hailstorms. Source: The Hindu BusinessLine, May 2026

| State | Procured 2026-27 (mt) May 12 | Procured 2025-26 (mt) same period | YoY Change | 2026-27 Target (mt) |

|---|---|---|---|---|

| All India | 30.15 | 29.17 | +3% ✓ | 34.50 |

| Punjab | 12.16 | 11.79 | +3% ✓ | 12.20 |

| Haryana | 8.46 | 7.05 | +20% ✓ | 7.20 (exceeded) |

| Madhya Pradesh | 7.04 | 7.77 | −9% ✓ | 10.00 (raised from 7.8) |

| Uttar Pradesh | 1.17 | 0.98 | +19%* | 2.50 (raised from 1.0) |

| Rajasthan | 1.61 | 1.55 | +4%* | 2.35 (raised from 2.1) |

| Bihar | 29,249 t | 16,655 t | +76% ✓ | 0.18 |

Impact on Fertiliser Imports

India is an energy deficit country. It relies heavily on other countries for imports like LNG. The disruption in supply from Qatar due to the US-Israel-Iran war has potentially impacted the import of LNG and consecutively, the production of Urea in the country. The extent of impact on Kharif can be analysed as we start getting the sowing data and the related crop growth data sets for Kharif in India.

LNG supply disruption from the West Asia conflict is squeezing India’s urea output just ahead of peak Kharif demand — adding input cost pressure to already compressed farm margins.

El Niño on the Horizon

Alongside the man-made disasters, a natural calamity is on the horizon. According to NOAA Climate Prediction Center, there is now a 61% chance of an El Niño forming between May to July 2026, which historically correlates with below-normal monsoon rainfall over India.

According to the IMD forecasts as of 13th May,

Monsoon advance forecast

- Week 1 (14–20 May): Southwest monsoon expected to advance over parts of south Bay of Bengal, Andaman Sea and Andaman & Nicobar Islands around 16 May 2026

- Week 2 (21–27 May): Further advance expected over south Arabian Sea, entire south Bay of Bengal, and parts of central Bay of Bengal

Week 2 rainfall outlook (21–27 May)

- Above normal rainfall likely over Central India, South Peninsular India, East & Northeast India

- Below normal over Western Himalayan region and plains of Northwest India

The below MSP price conditions across Rabi crops, a fertilizer supply squeeze, and a looming El Niño creates compounding risks. The interventions to increase the MSP for crops and procurement highlight the positive intent of the Government to stabilize the agricultural conditions.

Sources & References

- Down To Earth — “Harvesting of wheat almost complete yet government procurement has slowed”, Raju Sajwan, May 14, 2026. Accessed source for mandi vs. MSP price comparisons. Cites CWWG weekly report, May 11, 2026; CWWG report not directly accessed. downtoearth.org.in

- Food Corporation of India (FCI) — Wheat procurement data for RMS 2026-27 (state-wise), as of May 8, 2026. Accessed via Down To Earth and Whalesbook, May 14, 2026.

- Ministry of Agriculture & Farmers Welfare — Press note on MSP procurement approvals: gram in Maharashtra (limit raised to 8 lakh MT, >₹4,800 crore MSP value, window extended to May 29), May 5, 2026.

- Whalesbook — India Farmers Sell Below MSP as Wheat Procurement Stalls, May 14, 2026. whalesbook.com

- Whalesbook — El Niño 2026 Looms, India’s Rural Economy Shows Surprising Resilience, April 28, 2026. whalesbook.com

- Forbes — How the Iran War Impacts India’s Economic Fortunes, May 10, 2026. forbes.com

- Outlook Business — India’s Fertilizer Plants Shut Down as West Asia War Cuts LNG Supplies. outlookbusiness.com

- NABARD All India Rural Financial Inclusion Survey 2021-22. Source for rural household income composition.

- Ministry of Agriculture & Farmers Welfare — Second Advance Estimates, Kharif & Rabi 2025-26, March 10, 2026. Primary source for 3.2% Rabi growth (1,745.13 LMT vs. 1,691.66 LMT). pib.gov.in | ddnews.gov.in